Family and friends gather in San Felipe, Texas, for the Jan. 26, 2021, funeral of Gregory Blanks, 50, who died of Covid-19.

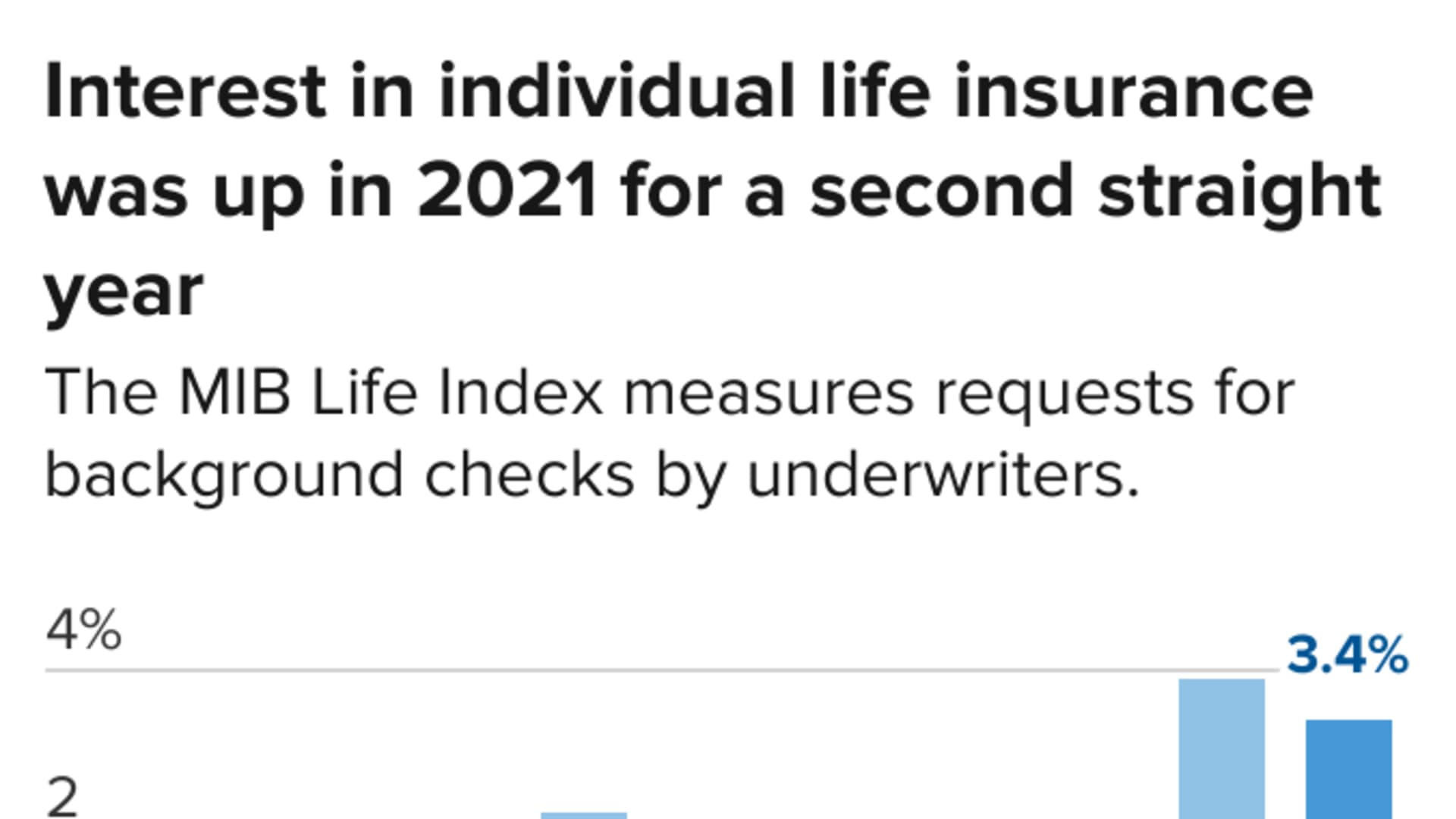

- Individual U.S life insurance application activity increased by 3.4% in 2021, following a record-breaking year-over-year growth of 3.9% in 2020.

- The industry is still wrestling with mortality assumptions related to Covid-19, and how shifts may affect the life insurance underwriting process.

- In the meantime, consumers may see Covid questions on life insurance applications, and experts are stressing why it's critical to answer truthfully.

As Americans brace for the third winter of the Covid-19 pandemic, many are still grappling with ongoing related health and financial issues — including insurance battles over long Covid treatments and disability claims.

WATCH ANYTIME FOR FREE

Stream NBC10 Boston news for free, 24/7, wherever you are. |

But for the life insurance industry, experts say the long-term effects aren't yet known.

"It's a work in progress," explained Michel Leonard, chief economist and data scientist at the Insurance Information Institute. "There's not enough statistical data at this point."

Get updates on what's happening in Boston to your inbox. Sign up for our News Headlines newsletter.

Faced with a staggering loss of life, insurance firms saw payouts soar during the pandemic.

U.S. life insurers paid more than $90 billion to beneficiaries in 2020, a 15.4% increase in payments compared to 2019 — the largest year-over-year jump since the 1918 influenza epidemic, according to data from the American Council of Life Insurers.

Money Report

Payouts to beneficiaries increased by nearly 11% in 2021, jumping to over $100 billion, the organization's latest report shows.

The demand for life insurance policies also jumped as consumers rushed to protect loved ones.

Individual U.S life insurance application activity increased by 3.4% in 2021, following a record-breaking year-over-year growth of 3.9% in 2020, according to the MIB Life Index's 2021 annual report.

However, the life insurance industry is still wrestling with mortality changes and how these shifts may affect the underwriting process.

There's still 'uncertainty' about mortality

Stuart Silverman, principal and consulting actuary at Milliman, an actuarial and consulting firm, said the Covid-19 pandemic has affected the life insurance industry in several ways, as outlined in a paper he co-authored in June.

Two areas of consideration are "mortality assumptions," which are projections of death rates and the "capital requirements" needed to keep life insurance providers solvent. Both can factor into the price of policy premiums, he said.

While it's clear mortality rates have increased since the beginning of the pandemic, experts don't know yet how factors related to Covid like preexisting conditions, compromised mental health or delayed care may affect future assumptions, according to the paper.

"I think there is uncertainty with how this will unfold," said Silverman, noting there's "ongoing debate" on many of these points.

How 'long Covid' affects mortality assumptions

Future mortality assumptions are murky for those who may be suffering from so-called long Covid, one of the terms used to describe lingering health problems after contracting the virus.

These conditions affect an estimated 7.7 million to 23 million Americans, according to a report released by the U.S. Department of Health and Human Services on Nov. 21.

"It's really difficult to underwrite for something that you don't have a clear way to diagnose and define," said Marianne Purushotham, corporate vice president and head of Limra's data services.

Overall, the life insurance industry is in a "major data gathering stage," Purushotham said, collecting information on all the ways Covid may be affecting mortality, including indirect effects like opioid overdoses and suicide rates.

She said one of the "big considerations" is whether impacts will be a long-term trend, noting that companies may not want to change pricing if mortality "settles into where it was pre-Covid."

"It's going to take five to 10 years for us to fully understand what patterns we're starting to see," Silverman added.

Applications may include Covid questions

While updates to mortality assumptions may take time, experts say life insurance applications have been quicker to change, depending on state regulations.

Consumer advocate Brendan Bridgeland, policy director and staff attorney at the Center for Insurance Research, has noticed Covid questions appearing on life insurance applications since the beginning of the pandemic and expects more in the future. For example, some companies ask questions about your history of testing positive for the disease and if you have a current diagnosis.

"States are still coming to grips with it," he said. "Companies have been quick to add application questions.

"But I don't think they've been perfected yet," Bridgeland added.

"While you may not see a vaccine question on a life insurance application yet, it's more likely two to three years from now," Bridgeland said. "I can see that on the horizon and I think that's going to be inevitable," he added.

"There are very big differences between the questions asked by life insurers right now," Bridgeland said. "Some make a lot of sense and others are very vague and slightly concerning."

With a lack of consistency across providers, he worries there's potential for consumers to misread a question and answer it incorrectly.

If a provider finds inaccuracies, there's a chance they will return your premiums rather than pay the death benefit to your loved ones, Bridgeland said.

To avoid mistakes, ask for clarification from an insurance broker or the provider, he said. "Just take your time, make sure you understand the questions and answer them truthfully," Bridgeland said.

Regulatory guidance is pending

In January 2021, the Consumer Federation of America sent a letter to the National Association of Insurance Commissioners, asking the organization to adopt a model rule for life insurance underwriters who may "delay or deny coverage" to applicants who have or have had Covid-19.

Prompted by life insurance underwriting changes in Europe, the Consumer Federation of America requested that the rules be "totally transparent" and "meet standards for reasonability" for applicants who may experience Covid-related delays or denials.

"This rule is also important for current policyholders who may be considering dropping their coverage for a period to save some money to help the family get through the economic consequences of Covid-19," the letter said. "These policyholders need to know the possible danger of such action."

The CFA also sent the letter to major life insurance companies, asking for them to "voluntarily make Covid underwriting rules public and reasonable."

While the NAIC addressed the letter during their spring 2021 meeting, the organization did not have enough information to consider supporting a model rule, a spokesperson for the National Association of Insurance Commissioners told CNBC.