Republican presidential nominee former President Donald Trump attends a rally at the site of the July assassination attempt against him, in Butler, Pennsylvania, Oct. 5, 2024.

- As 2025 approaches, top-ranked advisors are bracing for a looming tax cliff when trillions of dollars in tax breaks enacted by former President Donald Trump are scheduled to expire.

- The Tax Cuts and Jobs Act included several key individual tax law changes that could sunset after 2025, including lower tax brackets, higher standard deductions and a bigger estate and gift tax exemption.

- Meanwhile, advisors are focused on estate planning strategies and tax moves such as accelerating income and deferring deductions.

As 2025 approaches, top-ranked advisors are bracing for a looming tax cliff when trillions of dollars in tax breaks are scheduled to expire.

WATCH ANYTIME FOR FREE

Stream NBC10 Boston news for free, 24/7, wherever you are. |

Enacted by former President Donald Trump, the Tax Cuts and Jobs Act of 2017, or TCJA, brought a slew of temporary tax changes for individuals. Those provisions will expire after 2025 without action from Congress.

Some of the key changes included lower federal income tax brackets, bigger standard deductions, a more generous child tax credit, a 20% deduction for pass-through businesses and higher estate and gift tax exemptions, among other provisions.

Get updates on what's happening in Boston to your inbox. Sign up for our News Headlines newsletter.

It's unclear which TCJA provisions, if any, could be extended by Congress, particularly with uncertain control of the Senate, House and the White House.

In the meantime, some financial advisors have started tax planning for clients who could be affected. Here are some of their key strategies.

Money Report

Estate planning is a 'large focus'

Currently, there's a significantly higher estate and gift tax exemption under the TCJA, which allows tax-free transfers from wealthy Americans to the next generation.

In 2024, the lifetime estate and gift tax exemption is $13.61 million for individuals or $27.22 million for married couples. Next year, that limit will adjust for inflation before dropping by roughly one-half after 2025 if Congress does not extend the provision.

Transfers above those thresholds could be subject to a maximum tax rate of 40%.

"That's really been a large focus for us," said certified financial planner Peter Traphagen Jr., managing director of Traphagen Financial Group in Oradell, New Jersey, which ranked No. 9 on CNBC's 2024 FA 100 list.

Estate planning strategies leverage the exemptions to remove assets from the estate during life. However, techniques vary by family depending on their level of wealth, goals, life expectancy and other factors.

Plans can involve trusts, gifts to beneficiaries, direct payments to education institutions or medical providers, funding a 529 college savings plan and other tactics, said Shea Abernethy, an investment advisor representative based in Winston-Salem, North Carolina.

"Once it's out of your estate, it's not gaining interest or compounding," said Abernethy, who is also chief compliance officer for Salem Investment Counselors, which earned the No. 8 spot on the FA 100 list.

'Accelerate income' before tax hikes

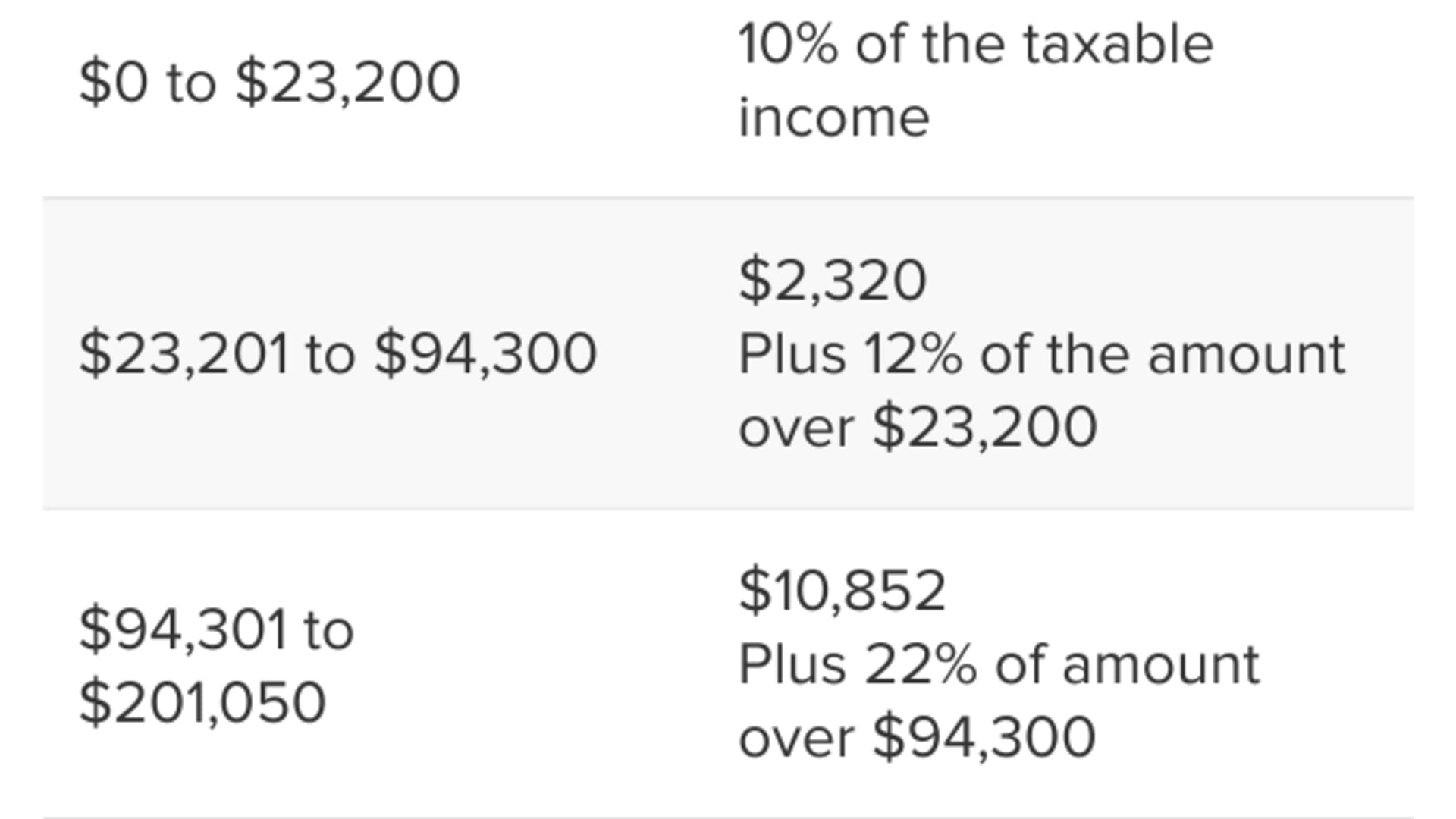

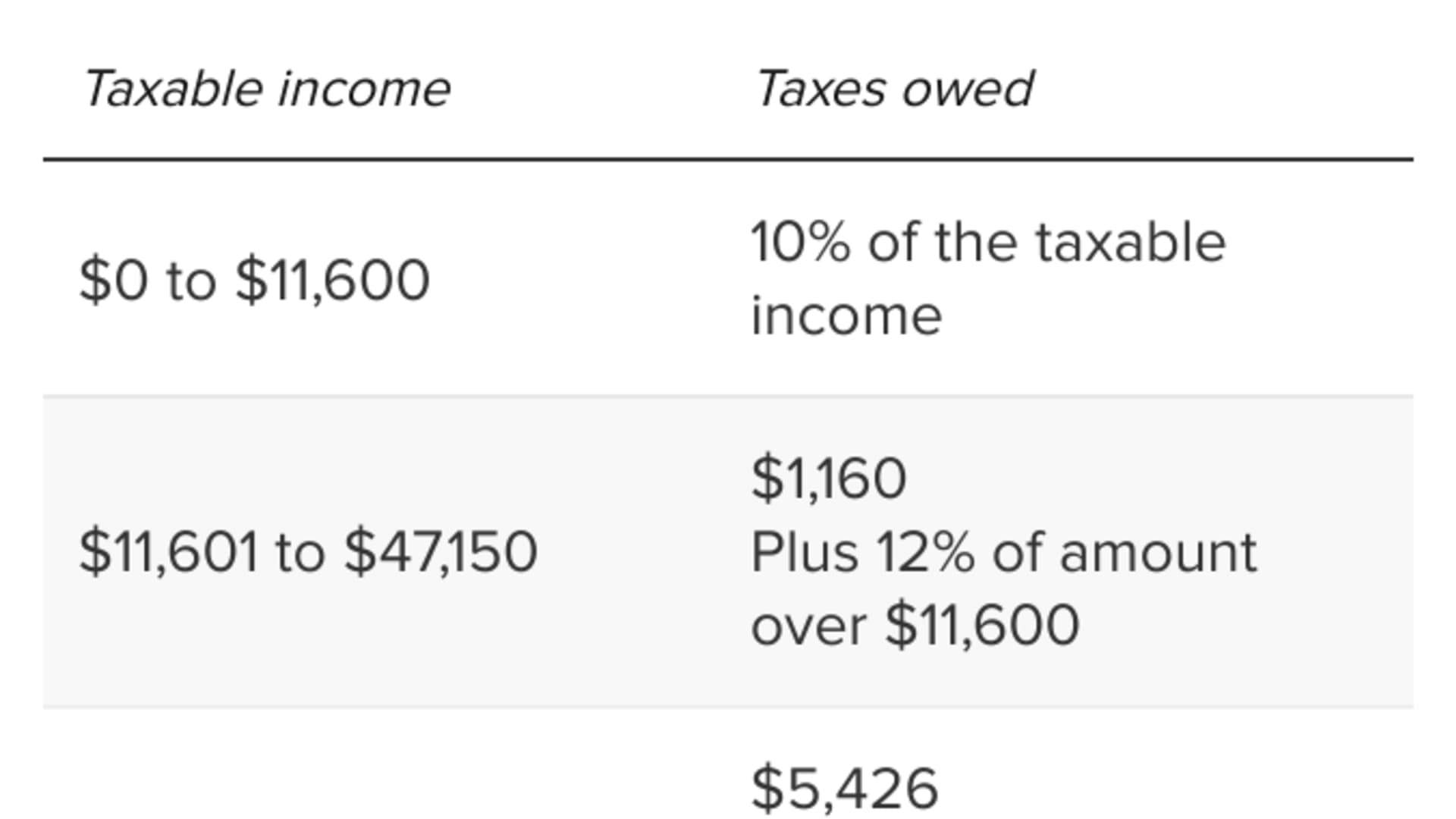

Some advisors are also planning for higher federal income tax brackets after 2025.

Without changes from Congress, the brackets will revert to 2017 levels, shifting to 10%, 15%, 25%, 28%, 33%, 35% and 39.6%.

"We are looking at strategies to accelerate income into the lower brackets now," said Samantha Pahlow, wealth management chair of Ferguson Wellman Capital Management in Portland, Oregon. The firm ranked No. 10 on the FA 100 list.

For example, that could include making Roth individual retirement account conversions or recognizing business income sooner, she said.

Pass-through businesses such as sole proprietors, partnerships or S corporations may also want to accelerate income to leverage the 20% qualified business income deduction, which could also sunset after 2025, Traphagen said.

Consider 'deferring deductions'

At tax time, filers claim the standard deduction or their total itemized deductions, whichever is greater. After 2025, they're more likely to itemize, if the standard deduction is cut in half.

For 2024, the standard deduction is $14,600 for single taxpayers and $29,200 for married couples filing jointly. That means most filers won't claim itemized tax breaks such as the deduction for charitable gifts, medical expenses, and state and local taxes, experts say.

But with a lower standard deduction scheduled for 2026, you may consider "deferring deductions," such as a donation to charity, Pahlow said.